In my last post, I discussed how Uber Eats and its potential acquisition of Grubhub might just be Uber’s savior. Well, this is just off the presses…Uber has failed in its takeover attempt of Grubhub. Just this morning, Just Eat Takeaway, a Dutch company, has agreed to acquire Grubhub for $7.3 billion.

In my last post, I discussed how Uber Eats and its potential acquisition of Grubhub might just be Uber’s savior. Well, this is just off the presses…Uber has failed in its takeover attempt of Grubhub. Just this morning, Just Eat Takeaway, a Dutch company, has agreed to acquire Grubhub for $7.3 billion.

The deal values Grubhub at $75.15 per share, a 27% premium to Grubhub’s closing price of $59.05. Apparently, this was one of the major roadblocks to Uber’s attempted acquisition of Grubhub. Uber was unwilling to pay the high price, and ultimately the two sides could not make a deal. Uber’s offer was closer to $70 per share, which would have valued Grubhub at about $5.9 billion.

The other major issue concerned regulatory risk, as I mentioned in part 1 of this post. Since Uber and Grubhub combined would have accounted for approx 50% of the US market, there were strong reservations about if the merger would get approval from antitrust regulators.

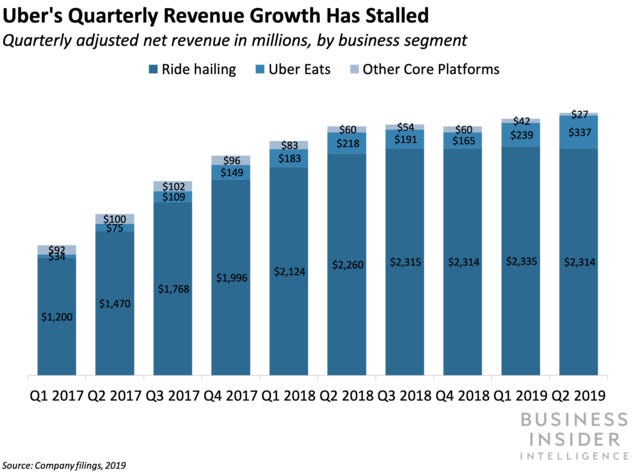

In a statement, an Uber spokesman said the company would continue looking for deals in the food delivery business, but would not engage in “any deal, at any price, with any player.” This begs the question, “what is the right deal, the right price, and the right player”? At the time of this writing, Doordash has 45% of the US market, followed by Uber Eats with approx 30%, Grubhub with approx 20%, and Postmates with approx 8%. Since Grubhub is no longer an option and a merger with Doordash seems improbable, the only remaining likely option is Postmates – probably not the ideal partner that Uber was looking for. Now instead of owning 50% of the market and being in a pole position, Uber would at best be looking at an equal footing with Doordash (see graph below).

Another equally troubling thing is that Doordash is backed by the “Bank of Softbank” which has poured huge amounts of capital that helped Doordash achieve its current market share. (Ironically, Softbank is also an investor in Uber; and investing in two competing food delivery companies is questionable strategy)

As we can see from the graph below, Uber Eats has not significantly increased its market share over the past two years, while Doordash has. And that increase coincided with Softbank’s investment in the company in 2018. As the graph also shows, Postmates’ market share decreased during the pandemic, which is troubling. At a time when food delivery businesses are doing a booming business, Postmates has lost market share. Granted, Grubhub also lost market share during this period (which may have contributed to their desire for a merger). And as you can also see from the graph, both of their losses equal Doordash’s gain.

In Uber’s Defense

In Uber’s defense, Just Eat Takeaway did pay a high price for the opportunity to expand to the US market. Normally, a 27% premium to the existing share price doesn’t seem too outrageous (most premiums fall within the 20-30% range). However, considering Grubhub’s declining market share (during the pandemic nonetheless), 27% does seem a bit high. Equally, if not more troubling would be the difficulty of getting the deal past the anti-trust regulators. So I can understand Uber’s not giving in and trying to negotiate a better deal.

However, Uber has been working on this year for one year, and it has to sting a little that they couldn’t get it done. For their sake, let’s hope it doesn’t turn out to be an even bigger failure and possibly even their demise in the long run.

#uber #ubereats #coronavirus #covid19 #ridesharing #businessstrategy #justeattakeaway #mergersandacquisitions #doordash #grubhub #postmates

What is your opinion? Feel free to contribute in the comments below.

Please feel free to share/repost/retweet